|

,We remain focused on our commitment to providing our clients access to care and easing their financial burden related to COVID-19. A new federal law expands how members can use their health savings accounts (HSAs), health reimbursement accounts (HRAs - Employee Pay), and flexible spending accounts (FSAs):

Employers don't need to do anything to make this change happen. It was made as part of the federal Coronavirus Aid, Relief, and Economic Security Act (CARES Act), which was signed into law March 27. It went into effect immediately. Here's an employer flier and an employee flier from ANTHEM, you can share, letting your employees know about the changes. We're steadfast in our commitment to support you and ensure our clients have affordable access to care. We'll continue to provide you with resources and updates related to COVID-19.

0 Comments

Coronavirus Aid, Relief, and Economic Security Act (Cares Act) Resources

Smart Choice® is thinking of our agency partners at this time. We will be compiling articles and resources on this page to keep you informed of the options available through this lending program. SBA Paycheck Protection Program and Economic Injury Disaster Loans applications open Friday, April 3 for small businesses and sole proprietors. Applications for independent contractors and self-employed individuals open Friday, April 10. It is important that you discuss these options with your local bank representative to determine your eligibility. Quick Links: Paycheck Protection Program sample application U.S. Department of TreasuryU.S. Senate Committee on Small Business & Entrepreneurship uschamber.com forbes.comustravel.orgtaxfoundation.org Lending Resources When Pat Kessler stepped up last year to provide help for an aging aunt after her uncle died, she had no idea what she was really in for.

Her aunt, 91, lives in her own home and wants to stay as long as possible. She is largely able to manage her daily needs, but has a history of falls and is vulnerable to being taken advantage of by others. Providing support was even more challenging because Pat lives in Minneapolis and her aunt lives in Denver. Through cross-country trips and frequent phone calls, Pat patiently worked to convince her aunt that she was there to help her. She also had to work on building trust and take the right steps to ensure her aunt had the local care and oversight she needed. And, like thousands of others, Pat had to do this while working full time at UnitedHealthcare® as a project manager. “Caregiving is much more work than I would ever have expected it to be,” Pat said, reflecting on her experience. “I don’t know how people do this — and I have a supportive manager and a fairly flexible job.” Navigating caregiving — one challenge at a timeOver about 8 months, Pat was able to persuade her aunt to agree to participate in a home assessment administered by a professional caseworker. The assessment evaluated her cognitive and physical needs, as well as safety issues in her home. Pat now helps manage her legal, financial and health care issues, and she hired a care manager to support her aunt’s needs locally. Despite building out a local care team, distance remained a significant concern for Pat. Her aunt now is part of a pilot program offered by UnitedHealthcare in 2019. Under the program, her aunt wears a personal emergency pendant that is connected to a monitoring center. If her aunt falls or presses the button on the pendant, it alerts the monitoring service to respond and arrange for help. The service also alerts Pat, providing her additional peace of mind. Although Pat accessed helpful resources through her employer to help guide her through the caregiving landscape, she still found herself juggling professional and caregiver responsibilities — an often difficult balancing act. “Part of the challenge with caregiving is that you need to make calls during business hours. You can’t do it at the end of the day or at night, because the people you’re trying to reach aren’t working then. For the majority of caregiving, between personal time and work time it’s extremely difficult to juggle.” Throughout the economy more and more workers double as caregivers As a full-time professional, Pat is not alone. One in 6 American workers—nearly 20% of the workforce — are engaged in caregiving roles. More than half of them work full time, and they spend an additional 20-plus hours a week providing care to another, usually an older adult.1 AARP® and the National Alliance for Caregiving (NAC) estimate that 43.5 million adults were providing unpaid care to an adult or child in 2015,2 and that the number of older Americans needing such care will grow to 117 million by 2020 as the baby boom generation continues to age.3 Moreover, many Americans are “sandwiched” between the needs of aging parents and their own children. In fact, 1 in 7 adults in their 40s and 50s provide financial support to both an aging parent and a child, according to the Pew Research Center.4 For employers, the consequences of this trend mean employees and their families are increasingly drawn into caregiving roles that can reduce their productivity. As a result, employees risk becoming so exhausted from the stress and strain of caregiving that it affects their own health. According to one study, caregiver absenteeism is costing U.S. employers up to $33 billion in productivity and $13.4 billion in increased health-care costs annually compared to non-caregiving workers.5 “Awareness and understanding of caregiving have been increasing among employers, lawmakers and consumers generally,” said Jim Murphy, vice president — innovation, Medicare & Retirement for UnitedHealthcare. “But many companies have yet to fully diagnose the root cause of productivity issues in their organizations, and at the heart of it many times are issues associated with caregiving.” Employer strategies to better support caregiversThe first step, according to Murphy, is to instill a more supportive company culture for caregiving. “Executives need to first acknowledge caregiving as a workforce challenge and foster a culture of support among managers so employees know it’s OK to talk about it,” he said. “Then, put in place caregiver-friendly policies and provide resources to support employee-caregivers.” Dr. Katherine Evans, chief nursing officer with UnitedHealthcare’s Retiree Solutions, says employers should take a page from a similar workforce challenge they’ve already tackled: child care. “Companies are clear on the importance of supporting their workforce with child-care resources and supportive policies. Caregiving can be as much or more work than child care. It can also be insidious, in that care needs often increase over time for older adults — and that takes a toll on caregivers,” she said. Dr. Evans said employers stand to gain tangible benefits by addressing caregiver needs. These include a more engaged workforce, better productivity through reduced absenteeism, retention of employees who might otherwise leave the workforce and healthier employee-caregivers, which can help “bend the cost curve” on a company’s total health care expenditures. Some examples of caregiver-friendly workplace policies employers may want to consider include:

Established in 2000, Solutions for Caregivers provides eligible UnitedHealthcare members, employees and retirees with access to a suite of supportive tools and resources. These include a Care Resource Center for coaching and support from caregiver advisors, information on community and government-funded programs to support caregiving needs, identification and screening of local public and private care services, as well as the development of personalized care plans and on-site assessments by care managers. “My aunt’s situation is better,” Pat said. “She is in a better place now than when I started caregiving 8 months ago. She still has challenges living on her own, but it’s rewarding for me to be able to go in and make an impact and hopefully improve her life at this stage.” Learn more about UnitedHealthcare’s Solutions for Caregivers,* and reach out to your Retiree Solutions representative with any questions. Sidebar: Coping with the challenges of caregivingNavigating a caregiving role carries many challenges. Most come to it unprepared. Although it can be fulfilling, it can also be lonely, frustrating and time-consuming. Sometimes all at the same time. Here are some tips from Pat Kessler, based on her own experience providing care to an elderly relative:

I found this great article from Entrepreneur Magazine. It's incredibly informative and intriguing related to using permanent life insurance strategies to help fund your business when banks won't. There are great tax advantages, interest rate advantages and improved control over your fiscal fitness. Check it out! When you're ready to learn more don't forget to call us at Unlimited Benefits. Experts in business coverage since 1998. Now offering complete package solutions for Employee Benefits and Business Liability and Property coverages.

Unlimited Solutions. Unlimited Service. Unlimited Control. 888.587.9370  Have you had an interest in getting benefits through your business but you have too many waivers, so participation keeps you from starting, or moving to a new plan. Maybe it's just too much trouble? Well, Health Net has decided to make it as easy as possible if your business would like to offer HMO benefits. For groups enrolling between 12/1/18 and 6/1/19 you can set up a health benefit account with Health Net with only an employer application, employee applications and a check! That is amazing! No need to turn in a DE9C or waivers or any of the other items that usually make benefit start up difficult. See below!

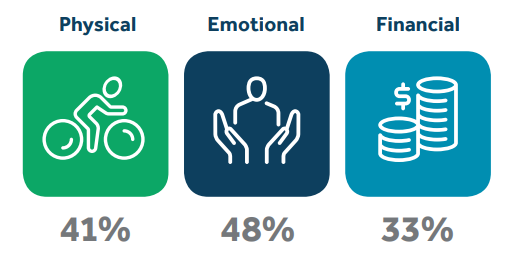

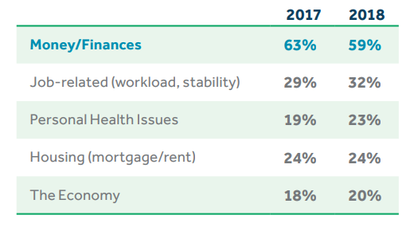

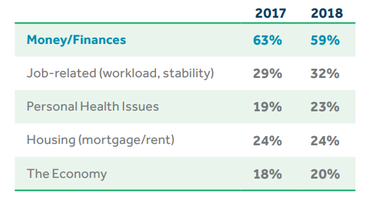

Call Unlimited Benefits today to get started with your new employee benefit program. Proposal are free! Call now: 888.587.9370. More than twenty years working with businesses from 2 to 2000. Like most Americans, small business workers want less stress and better work-life balanceBenefits offered by small firms contribute greatly to the financial, physical and emotional wellbeing of America. Guardian’s latest Workforce Well-being Index reveals that employees of small firms have an Index score of 6.5 on a 10-point scale, virtually the same as the 6.6 average for all working Americans. However, the financial wellness component of the Index is low among small business workers, and is lower when compared to employees of large companies. % Rated excellent/very good health by small business workers Money is the primary stressor for small business workers. Six in ten cite personal finances as the top source of stress in their life. That is nearly twice as many as those citing job-related concerns and three times as many as those mentioning personal health issues, housing costs or the economy. The well-being of 60 million Americans is linked to small businessesTop Sources of Stress: % of small business workers Workers place a high value on their time: time to care for themselves and their loved ones. Greater flexibility in how, when, and where individuals work is becoming a very desirable benefit, and is a factor in attracting and retaining talent, especially in competitive labor markets. Workers Seek Employer Support on Wellness% of small business workers who strongly agree Half of all small business workers feel that their employer cares about their overall well-being, which is an improvement over 2015. That’s important because those who believe their employer cares about their overall well-being are more loyal; they are 1.7 times more likely to prefer to stay with their company for at least 10 years compared to those who don't feel their employer cares. The information above was taken from the 5th Annual Guardian Workplace Benefits Study.

Download a copy today -> Guardian Workplace Benefits Study Unlimited Benefits, Inc. is always striving to stay at the forefront of industry changes and events. Call us today to learn how we can help you increase your employee satisfaction. 888.587.9370  Personnel Files

It’s easy to assume that the storage and maintenance of employee files is quite simple. However, they have a bit more complexity to them than one may think. We’ve worked with several employers to have the best practice of grabbing a file, throwing all employee-related documents into it, storing the file alphabetically and viola; it’s done. Could that be you? If it is, you could be opening yourself up to avoidable risk. Have no fear, we are here to help you get your files up to par. There are three employee related files that an employer must maintain to ensure that you are legally compliant in your record keeping • General Employee File • Medical File • I-9 File The organization of documentation within each file is primarily up to you. However, different guidelines are associated with different employee file types, which we will review shortly. Before we get started, here are a few general accessibility and security measures that should take place to ensure that you are handling sensitive information correctly. • Access to a personnel file is restricted to certain employees in most organizations. To provide optimal security of your employee's sensitive data, we recommend limiting access to your selected HR representative and business owner. • Generally, employee access to his or her personnel file is allowed. But it is recommended that you create and distribute a policy outlining guidelines regarding file access. Many states have their regulations regarding this topic. • Most organizations do not allow the employee's manager to access employee files. They expect the managers to keep relevant documentation in their employee file which is not the official personnel file. • All files must reside in a safe, locked, inaccessible location. The file cabinet that houses your three files should be separate from each other. The filing cabinet must lock, and your chosen HR representative should have the only keys. Required Files Let’s take a closer look at each required file and how to properly maintain them. Employee Personnel File This is the main personnel file an employer maintains for each employee. The personnel file stores the employment history of each employee. What’s in this file- Application and resume, documentation of employment history, records of contribution and achievement, disciplinary notices, promotions, performance development plans, performance evaluations, and much more belong in a personnel file. Documentation is necessary, so you have an accurate perspective of the employee's history. When you keep the right documentation stored correctly, you will ensure that you are protected against any legal action or issues. When you can demonstrate your rationale behind hiring, promotions, transfer, rewards, and recognition, and firing decisions through solid documentation and filing practices, you can sleep soundly. Medical Files The employee medical file has legal restrictions that the employer must know and heed. The employer must keep a medical file separately for each employee to ensure compliance with the Health Insurance Portability and Accountability Act of 1996 (HIPAA). HIPAA requires employers to protect employee medical records as confidential; medical records should be stored separately from other business records. Never store employee medical records in the employee’s general personnel file. What’s in this file- The employee medical file is the repository for everything that has to do with health, employee health-related leave, and benefits selections and coverage for the employee. This includes doctors notes and medical leave paperwork. I-9 Forms File The Form I-9, Employment Eligibility Verification is the form that is required by the Department of Homeland Security and U.S. Citizenship and Immigration Services (USCIS) to prove an individual’s eligibility for employment in the United States. An I-9 must be completed for every employee. Essentially there are two steps to completing the I-9: 1. The employee must complete section 1 and provide you with original identification that is listed on page 3 of the I-9. 2. The employer must complete section 2 within three days of the employees first day on the job and attach copies of the identification provided by the employee. The form verifies that you have reviewed the approved forms of identification that prove the employee is legally authorized to work in the United States. There are some nuances to completing the I-9. To ensure that you are completing the I-9 correctly, check out the USCIS (US Citizenship and Immigration Services) Handbook for Employers for more information. Click HERE to access the employer's the handbook. To properly store and maintain this document, you will want to keep all employee I-9s, and the accompanying documentation separate from other files. The government may audit these forms. In the event of an audit, keeping your I-9s filed separately will ensure that you maintain company and employee confidentiality. While it seems that managing three separate files could be quite cumbersome and time-consuming, it is easier than it seems. Having separate personnel, medical and I-9 files will help you to stay organized, compliant and secure. This will result in professional best practices that allow you and your team to focus on what you do best- growing and running your business. Managing employee files is just the tip of the iceberg when it comes to small businesses and their HR needs. HR Branches is here to help you take your HR from Hassle to “Handled!” Check out www.hrbranches.com to learn more how about how our cost-effective solution can help you gain some peace-of-mind today. **HR Branches provides general information about Human Resources. Please note that the information provided, while reliable, is not legal advice. Please seek legal assistance, or assistance from State, Federal, or International governmental resources, to make sure your legal interpretation and decisions are correct for your location and circumstances. Guest Post provided by: Reanna Werne, HR Branches Thanks, Reanna, for the excellent information! Successfully motivating your employees will help you achieve and maintain business goals. Ultimately, you want to create an environment that allows your employees to meet or exceed expectations, do their best and feel valued. While employees are clearly motivated by tangible rewards such as salary and promotion, there are more intangible factors such as mentoring, personal and professional growth and the ability to work on independent projects.

Motivational Drivers We are all individuals with different needs and aspirations, so what motivates one employee may not motivate another. Creating a work environment which includes a range of motivators can result in improved performance as well as increased retention and enthusiasm for the company. The following is a brief summary of different motivators:

These strategies may motivate your employees to contribute to your businesses performance:

Effective immediately Health Net now considers employees enrolled in an IFP (Individual & Family Plan) plan as VALID WAIVERS.

IFP members who do not enroll in a group plan because they are already insured (with IFP coverage) no longer count against group participation! This is very important. If you've been denied coverage because your group's participation was too low you now have the opportunity to finally get the coverage your business deserves! Get a quote for your business today!! The door just swung wide open.

As always, Unlimited Benefits is here to guide you in all your employee benefit needs. Reach out let's see if your group with generally low participation can finally be approved! IRS Established 2019 HSA Guidelines

Below is an overview of the IRS inflation adjusted HSA dollar limits for calendar year 2019 as published in Revenue Procedure 2018-30. Minimum HSA Qualified Health Plan Deductibles for 2019 (no change from 2018): • Self-Only Coverage: $1,350 • Family Coverage: $2,700 (includes embedded individual deductible on a family coverage plan) Maximum HSA Qualified Health Plan Out-of-Pocket Limits for 2019: • Self-Only Coverage: $6,750 (increased from $6,650 in 2018) • Family Coverage: $13,500 (increased from $13,300 in 2018) • Out-of-Pocket limits include deductibles, coinsurance and copayment amounts, and excludes premiums IRS HSA Contribution Limits for 2019: • Self-Only Coverage: $3,500 (increased from $3,450 in 2018) • Family Coverage: $7,000 (increased from $6,900 in 2018) • Catch Up Contributions (for individuals age 55+ until enrolled in Medicare): $1,000 (no change from 2018) Contact Unlimited Benefits at 888.587.9370 for more information |

Clint Perry

Founder of Unlimited Benefits and Financial Services Expert since 1994 Archives

April 2020

Categories |

RSS Feed

RSS Feed